What you need to know about simplified RMB cross-border trading

By Nathan Chow Hung Lai (周洪禮)On 10 July, the People’s Bank of China (PBoC) announced a series of measures aimed at simplifying renminbi (RMB) cross-border transactions.

We highlight three key measures and the respective implications to the market.

1. Based on the basis of ‘know your customer’, ‘know your business,’ and ‘due diligence’, banks in the mainland can process RMB cross-border trade settlement for their corporate clients before verifying the documentary proof of underlying trade transactions.

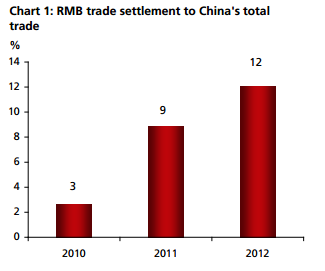

Beijing launched the RMB cross-border trade settlement pilot scheme in 2009 and gradually expanded it to cover trade between all Chinese provinces and foreign countries. In 2012, the proportion of China’s trade settled in RMB quadrupled to 12% from 3% in 2010 (see Chart 1).

Overall, the improved streamlined process will increase the efficiency in handling RMB-denominated trades. This should, in turn, increase the adoption of the RMB for trade transactions globally.

To simplify the procedure for corporate use in RMB, the PBoC also approved a new scheme in March to make it easier for a European Fortune 500 company with substantial sales in China to manage its RMB holdings.

Before the new model was introduced, the company had to process multiple cross-border RMB payments separately for regulatory oversight, resulting in transaction costs and a lack of central monitoring. Some domestic banks were also frustrated that settling trade separately had been both time-consuming and labor intensive.

To address the above concerns, a new scheme — gross-in/gross-out arrangement — was introduced. The company can consolidate all incoming RMB transactions made in different time periods into a single transaction; as well as all outgoing RMB payments into another.

This centralized approach to cash management significantly reduces the exchange rate exposure and optimises liquidity management for the company. It also sets a precedent for other foreign corporates to adopt the RMB in international trade.

There is some worry that the authority’s efforts to promote the international use of the RMB is dependent on the appreciation expectations for the currency.

We do not share this view.

For corporations trading with China, the use of RMB can lower their FX costs and risks. They can also enjoy the price discounts offered by some Chinese companies. That explains why currency appreciation or depreciation might be less relevant from a supply chain perspective. Cost advantage is the main driver that fuels the growth.

2. Non-financial companies can use the RMB fund held within their organizations in China to extend loans to their overseas affiliates.

This was one of the policy initiatives that we expected would be launched this year (see, “CNH: Replenishing offshore RMB liquidity”, 13 Dec 2012).

To recap, with a more balanced RMB inflow and outflow via the trade channel, there was a need to develop other avenues to replenish the offshore RMB liquidity pool. This requires the mainland to expand the focus of RMB reforms from current account to capital account convertibility.

Currently, ten out of the forty specific items under capital account transactions in China are classified by the IMF as tightly restricted. The rest of the items, to a certain degree, are considered as convertible.

The degree of openness for direct investments is the highest amongst all. The items that are still strictly controlled are related to cross-border transactions in capital market and financial instruments.

Hence, the next stage of liberalizing the capital account is to allow overseas and Chinese entities to engage in cross-border asset transactions. The latest initiative allows onshore non-financial companies to better utilize excess RMB liquidity to fund related offshore business, which is consistent with the “Going Out” strategy promoted by the central government.

The new rule also encourages overseas M&A activity, especially to promote RMB outward direct investment (ODI), which has lagged behind its inward counterpart (see Chart 2 at the bottom of this article).

3. For non-financial companies that plan to issue RMB-denominated bonds in the offshore market, they can set-up a special deposit account at a domestic bank to keep the remitted proceeds raised via the bond issuance.

In mid-2012, the National Development and Reform Commission (NDRC) released a set of rules standardizing the process for offshore RMB bond issuance by onshore non-financial entities. Guidelines included the minimum criteria of eligibility, application procedure, documentation requirement for collateral/guarantee, and the response time of the NDRC after filing of application.

The latest arrangement complements the existing regulatory framework governing offshore RMB bond issuance by Chinese corporates. Facilitating the development of the offshore RMB bond market has been part of Beijing’s effort to liberalize the mainland lending environment, which is currently dominated by indirect financing (bank loans, policy rates) rather than direct financing (bond issuance, market rates).

Nevertheless, the latest policy change would not induce a significant increase in Chinese corporate bond issuance in the near term. Specifically, no changes have been made regarding the remittance process and usage of proceeds.

According to the current regulations, proceeds need to be deployed mainly in fixed asset investments, and must comply with the country’s macro-control policies, industrial policies, foreign capital utilization, and foreign investment policies.

Of equal importance, offshore funding costs have become comparable to those of onshore. Since June, the weakening RMB appreciation expectation amid moderating mainland economic activities has already pushed offshore bond yield sharply higher (see Chart 3 at the bottom of this article).

Also, the recent liquidity squeeze onshore will possibly generate more interest among Chinese companies for borrowing from Hong Kong banks. The resulting higher offshore funding costs might in turn dampen the appetite for issuing offshore RMB bonds in 2H13.

Advertise

Advertise