Sponsored Articles

123RF bets on casual creatives with cloud tech M&A

123RF bets on casual creatives with cloud tech M&A

Known for its affordable stock photos and digital design assets, Inmagine Inc’s 123RF is betting big on the casual creative market with its acquisition of Autodesk’s popular Pixlr family of digital editing apps.

PayCommerce's Shekhar Nair to discuss his take on the current status of cross-border payments

Nair is one of the speakers at the 2017 Retail Banking Forum in Jakarta.

Rajiv Madane of Fiserv to speak at the Asian Banking and Finance Retail Banking Forum in Jakarta

His presentation will cover the next-gen customer experience journey in payments.

Fiserv's Rajiv Madane to talk about solving business challenges through innovative card and payment solutions

He always tells clients to "think broadly, look far".

Experian executives to share insights on "online only" banks, AML at the ABF Retail Banking Forum Manila

Find out more about Sujatha Venkatramanan and Burak Alper.

Five financial self-service trends you cannot afford to ignore

Omnichannel experiences will soon become standard operating procedure.

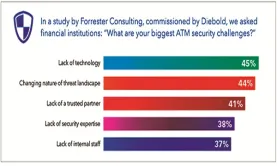

New Forrester research on ATM Security: How prepared are you?

Find out what challenges retail banks are facing in managing the security of their ATM fleets, as well as security strategies and programs to overcome them.

SmartStream slashes cost of trade breaks due to bad data by around 90%

Three of the world’s biggest banks – Goldman Sachs, JPMorgan Chase and Morgan Stanley – are now founding members of SmartStream’s Reference Data Utility.

OCBC Al-Amin reaching out through Xpres branches

Islamic Banking is gaining popularity among not only Muslims but non-Muslims as well in Asia. On its part, OCBC Bank sees this as an opportunity to offer an even broader array of competitive and innovative financial products and services to consumers and businesses. And it recently started doing so through the Xpres branches of its Islamic banking subsidiary, marking a milestone in the four-year journey of OCBC Al-Amin Bank Berhad.

Adapting to changes in business demands while improving growth and operations

Infor understands that competition among enterprises is more than just tough, thus it steps in to provide innovative systems and flexible solutions to give companies the leverage they need.

MIT brings CREDOC and TRAC to Asia

Check out MIT’s premier products for Asia’s trade commodity finance industry.

Maximizing benefits of card networks

MasterCard reveals pieces of advice for companies on getting the pros and hedging the cons on key banking trends.

Trade Forex and save your time

Find out how you can trade on the market with less time and effort yet take as much profit as experienced traders do.

A rising dragon in the ATM industry

China’s phenomenal economic growth over the past three decades has attracted much attention worldwide.

Are you losing GEMS?

Companies must not lose emails from their customers, suppliers and partners.

3i Infotech talks about the LRI process

The banking world hasn’t been as dynamic as we see it today and bankers are looking at technology as an enabler to meet up with the challenges of ever changing banking industry. The current downturn has lead to banks no longer having the luxury of deep pockets, extended timelines or telling their customers to be patient while they go through a refurbishment of their systems. The world is here and now. This then is crunch time. The marketplace is demanding “more for less”. Banks need to offer more products and services than their immediate competitors, faster, cheaper and more conveniently. On top of that, the silos of banking, insurance, wealth management, mutual funds, and mortgage companies are becoming one big banking melting pot. Bankers are very adept on knowing exactly what their end customers need, but they do not really know how their technology infrastructure will support them on their customer needs. The legacy systems are good enough to “run the bank”, costly yes, but good enough, but they are no good if the need of the hour is to “change the bank”.Faced with the growing competition from the marketplace, and the need to keep up, banks and their solution providers have been forced to move away from the “big bang” change of core systems. Instead they are adopting the process of “Legacy Replacement by Installments” (LRI) which enables banks to replace specific segments of their systems in a time-bound and effective process. LRI helps banks operate their existing systems while upgrading a component. The new components based on service-oriented architecture seamlessly operate along with the older systems, thus making it time and cost-effective for the bank, and effortless for the bank’s existing customer community.To enable fast, effective LRI, we need to keep the following criteria in mind:1) The components must be SOA compatible so that their end results become paramount, measurable and congruent.2) The new system must afford express customization, as this is the key to the bank having unique offerings, and to offer products that best harness its differentiated business processes.3) The customer experience must be totally unique and give a very different comfort feel, through whatever channel the customer chooses to interact with the bank, and be equally comfortable to customers who are established, as well as those who are relatively recent additions.4) The technology should afford scalability so that the bank does not run out of capacity, as and when the product launches succeed in the marketplace.5) The system should be easy to integrate across a galaxy of disparate systems, and must work seamlessly with the existing products and services, because the bank’s goodwill does depend on the existing customer community.LRI can be looked at one of the pragmatic ways for bankers aspiring to retain and enhance their competitive edge. If drafted carefully, LRI program can a long way in helping bankers achieve the supremacy in technology. Following are some of the pointers, which can be looked upon as to increase the effectiveness of LRI : 1) The bank’s management must involve IT proactively before major business decisions are taken – not as an afterthought.2) Banks cannot afford to proliferate more silos in order to support business growth.3) Banks have to find a way out to not only rationalize applications that perform similar functionality within the organization, but also identify, isolate and reuse business logic and data that represent core business processes such as account origination and pricing.4) Banks cannot afford to hold onto applications that rely on outdated technology.5) Banks must have consistent processes across the lines of business for similar functions.6) Banks must invest in obtaining a holistic view of the customer across the product silos.7) Banks must move away from vendor lock-in situations by moving to a service-oriented architecture and standards-based interfaces.8) Banks must measure the return on additional technology investments more closely and in terms of impact on business agility and performance.Therefore, in conclusion, the banking world is no longer ready to wait more than one quarter to see the impact of its technology investments. This makes it imperative for the technology partner to enable existing technology and systems to effectively and seamlessly interact and co-exist with the new technology. The chances that partners will be able to land orders for a completely new comprehensive retail banking system are dimming by the minute. No bank can afford that type of money, the enormous disruption to existing processes and customers, or the extended time-table that such a change envisages. Legacy Replacement in Installments is a methodology that reduces the “shock effect” to the existing infrastructure, and is relatively affordable and time-efficient.

Thought Leadership Centre

Resource Center

Advertise

Advertise

Event News

Monitor Deloitte's Prashant Krishnan urged banks to transform their relationship models to meet these demands.

Commentary

Asian firms need to get ready for digital assets and currencies

AI can build your plan, but can it hold you to it?

Built to last: How Japan is approaching the cross-border payments challenge