Banks feel pressure from private credit

Nonbank lenders are now providing capital even to low-risk corporate clients.

Private credit has become a recognised asset class and is now a common part of institutional investment portfolios, amidst declining profits in Asia-Pacific banks, shifting valuations, and competition from fintech.

Traditional universal banks are increasingly squeezed between nimble digital competitors and high-value niche players, Isaac Tan, a partner at Boston Consulting Group in Kuala Lumpur, told the Asian Banking & Finance and Insurance Asia Summit - Malaysia 2025.

"Private credit players are entering a space that banks traditionally serve. But because of regulation, banks are moving away," he pointed out.

Nonbank lenders—typically credit fund managers who work directly with corporate borrowers—are now providing capital even to low-risk segments that were once the exclusive clients of regulated banks, he added.

To maintain a presence in these markets, some banks have opted to become investors or partners in private credit deals—a strategy that is becoming more common in markets such as India, Tan said.

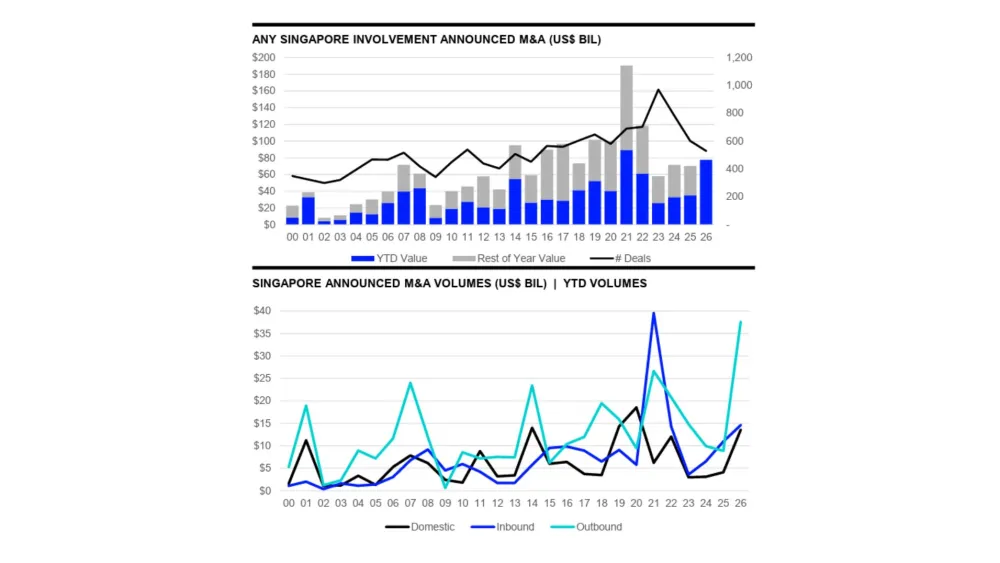

The Asia-Pacific private credit market was valued at about $120b at the end of 2023, with a sixfold increase in assets under management from 2014, according to London-based investment data company Preqin Ltd.

Since the 2008 global financial crisis, banks’ return on equity (ROE) has steadily declined across most markets.

India’s last best ROE dates back to 2013 at 14.9%, whilst China’s best was at 20.6% back in 2011, Tan said. Both Japan and South Korea’s highest ROE dates back to 2010 at 11.8% and 13.2%.

In the Philippines, digital banks already account for 9% of the total market capitalisation of the banking sector, and serve 45% of the average customer base handled by the country's top three traditional banks, he added.

Tan said that Malaysia is likely to see a similar shift soon.

Regulations are also pushing banks to retreat from segments where capital is inefficient, allowing private credit providers to move in.

Whilst some banks are adapting and gaining value, others risk falling irreversibly behind.

As of last year, banks in many regions were valued below their book value, a signal that investors doubt their ability to deliver superior returns, Tan said.

However, banks are not losing ground equally.

Tan noted that whilst overall valuations have risen slightly in recent years, the gap between high-performing and underperforming banks has widened.

"The winners are getting wealthier, and the laggards, you see the increasing deviation as well,” he said. “This divergence is no longer a matter of perception; it is a structural trend.”

One of the most significant drivers of this shift is the rise of focused models—financial institutions that concentrate on specific customer segments or services.

"On average, the focused models, the better ones, tend to have two to six times better valuation than the better performing banks,” Tan said.

Advertise

Advertise