Singapore

UOB's net profit up 5.4% to US$578m in Q1

And NPL was stable at 1.5%.

OCBC's Q1 net profit expected to decline 4% to around US$586m

Provisions will remain high for the same O&G accounts.

UOB's ROE to outperform peers in 1Q17: analyst

But core net profit is seen to grow only 3%.

Singapore banks' loan growth to be 'relatively subdued'

That is despite a slight recovery in February.

Singapore's big 3 banks to post lacklustre earnings for 1Q17

Net profit of two banks will decline, whilst that of one bank will remain flat.

Singapore banks' ROEs to stay depressed at 8-9%

NIMs are expected to remain muted with only a 1-2bp pickup.

Bahrain follows Singapore's footsteps to become regional fintech hub in the Middle East

The first Middle East and Africa Fintech Forum is but a start to its fintech plans.

Adam Proctor named Citi Private Bank's head of managed investments and advisory for Asia Pacific

Adam Proctor will take over the role of Head of Managed Investments and Advisory for Asia Pacific, reporting to Roger Bacon, Head of Investments for Asia Pacific and David Bailin, Global Head of Managed Investments. He will relocate to Singapore in the coming months.

Here's why the 2017 Asian Banking and Finance Retail Banking Forum Singapore is worth attending

The event will be held on April 26 at the Pan Pacific Singapore.

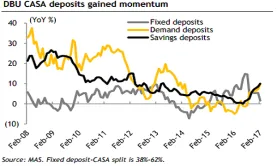

Chart of the Week: Singapore banks' domestic banking unit CASA deposits gain momentum

Banks in Singapore continue to offer attractive rates.

Weekly Global News Wrap Up: Goldman Sachs, Bank of America report increased profits for Q1; Wells Fargo tests Facebook chatbot

And find out how regulators risk putting banks on a fast track out of London.

Asian private banks' assets under management reach record high in 2016

AUM increased 6.1% to $1.55t in 2016.

How will banks' branch services be led by digital?

Find out why branch transformation depends primarily on technology.

DBS, OCBC to enable QR code payments

Payments can be made on NETS terminals.

ICBC Singapore launches dual currency credit card

It carries SGD/RMB dual currency functions.

Banks caught in a social pickle

If incumbent Asian banks should be wary of fintech firms, it is not because of the disruption they can cause. Rather, fintech firms can steal the entire customer relationship from banks, and basically profit from the hard work that banks put in to keep clients engaged.“Not a lot of fintechs want to disrupt banking actually. What they want to do is disintermediate customer relationship,” says James Lloyd, Asia-Pacific fintech leader at EY. “This is because most of the profit accrues to the people who own the customer relationship, not to the people who manufacture the product.”A worrisome trendHe reckons the trend of banks increasing their presence in social media and messaging platforms like WeChat is worrisome. Banks run the risk of eventually conditioning their clients to depend on the fintech platform rather than the bank itself.“All the banks have integrated with WeChat specifically to enable people to check balances and so on through the messaging app. At a certain point, the customer relationship then becomes with the intermediary, not with the bank,” says Lloyd. “Financial institutions will integrate into messaging platforms and social but then they lose their customer relationship.”Despite this threat, banks are still teaming up with popular messaging apps and other payment providers to leverage on the latter’s strong digital presence. Citi, for example, has plugged into WeChat and Alipay in China, allowing clients to receive alerts, make inquiries, and even repay their Citi credit cards using their Alipay account, given that 95% of the bank’s transactions in the country happen outside the branch. Banks and social mediaHua Zhang, analyst with Celent’s Asian financial services practice, says banks may not have much of a choice but to dive into social media due to the breadth of benefits that these digital spaces offer.He adds that for traditional banks to leverage social networks to develop banking services, simply opening a Facebook account is far from being enough. Generally, banks may follow three steps to establish social banking: First is customer acquisition, which is to construct a platform in social media and leverage user traffic in social networks to reduce costs and acquire users. The second one is customer segmentation, which is to segment customers into closely defined groups and provide professional online and offline services to them. These services, says Zhang, are generally not financial services, but rather integrated services such as overseas services, automotive services, and so forth. Lastly, customer conversion, which entails directing the users to become customers of the bank with a demand for financial products.“Social networks enable banks to come into closer contact with customers and carry out effective customer segmentation, thus allowing them to provide better consumer finance, payment, and other services,” notes Zhang.

Thought Leadership Centre

Most Read

1. Leading banks, financial companies lauded at Asian Banking & Finance Awards 2025 2. UOB acknowledges penalty for anti-money laundering breaches 3. OCBC Bank (Malaysia) Berhad recognised at Asian Banking & Finance Wholesale Banking Awards 2025 4. Standard Chartered faces legal battle over $2.7b fraud claims in 1MDB case 5. Revolut partners with Ant Int’l to enable transfers to China via AlipayResource Center

Advertise

Advertise

Event News

The financial institution emerged as the recipient of the Green Deal of the Year - China and Green Deal of the Year - Singapore awards.