Singapore

Why Singapore banks won't be surprising analysts with impressive gains

Blame it on volatile capital markets.

Hong Kong overtakes Singapore as Asia’s premier wealth management hub

The Lion City is a ‘stagnating’ centre, says Deloitte.

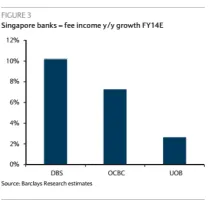

Chart of the Week: Singapore banks to suffer from weak market-related income in 4Q14

Also, trade loans could fall faster than expected.

DBS’ net profit up 10% to $3.8b in FY14

On back of higher NIM, loan volume and fee income.

Here's why 2014 was a challenging year for Singapore banks' loan growth

Growth across the board was sluggish.

Why Sibor's 16bp advancement in 2015 is "unusual" in Singapore

Versus other liquidity-rich markets.

Singapore banks lauded for strong funding franchise

Thanks to rocketing household savings.

Singapore banks' core earnings growth predicted to jump 10% in 2015

Banks are impressively geared up for headwinds.

Singapore banks brace for more delinquent property loans

As shoebox flats flood the market.

Why rising interest rates don't hail the start of "big interest rates upturn" in Singapore

Some considerations must be made, analysts say.

Singapore's UOB sues Lippo, 7 other firms over home loan anomaly

Loans for 37 condos have defaulted.

Singapore banks’ hiring intentions plunge on back of weak market outlook

But compliance and regulation roles are in demand.

OCBC feared to be at highest risk in any housing meltdown in Singapore

Should it feel very afraid?.

Which bank in Singapore is susceptible to unchanged interest rates?

This involves the SGD SIBOR as well.

Only 39% of banks confirm payments in real-time: survey

A lot more progress is needed.

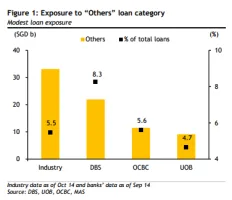

Are Singapore banks dangerously exposed to the fallout from cascading oil prices?

The banks could be affected in an industry shakeout.

Thought Leadership Centre

Most Read

1. Citi expands AI rollout to Indonesia 2. Nine in 10 investors do not trust AI for investment decisions 3. SCB rolls out 24/7 USD clearing in Thailand with Citi Token Services 4. UOB and ANTA sign MOU for cardholder discounts 5. HSBC pilots digital structured product issuance in Hong KongResource Center

Advertise

Advertise

Event News

Banks can respond by moving toward a hybrid advisory model.

Commentary

How alternative data lending is reaching Southeast Asia's unscored MSMEs

Asia is leading payments modernisation and banks can't afford to fall behind

Investing in an inefficient market

Platinum cards, paper-thin compliance?

Energy price volatility highlights structural gaps for managing FX risk in APAC