Singapore

Asia Pacific's wealth management sector mired in massive challenges

Asia Pacific's wealth management sector mired in massive challenges

Asia Pacific has overtaken North America for the first time as the region with the highest number of high net worth individuals (HNWI), 3.37 million in 2011, according to the latest World Wealth Report, jointly published by RBC Wealth Management and Capgemini, and this figure is set on an upward trend. Welcome statistics for wealth managers. Saying that, this explosion in the HNWI segment can also present a thorny challenge for the industry.

It's high time to educate the new generation of retail bankers

The banking model is fatally flawed. It’s time to break up the universal banks, separate the cavalier commercial arm from the retail element, and educate the new generation of retail bankers.

The impact of fragmentation and complexity on AsiaPac banks

Banks across Asia Pacific continue to wrestle with issues surrounding corporate actions processing. Changes to the distribution of event notifications – often still inconsistent and fraught with delays that increase risk and operational costs – have long been overdue. However due to the fragmented nature of the Asia Pacific region, creating a standardized approach to overcome these problems is a significant challenge.

Here's all you need to know about BofAML's new CashPro Accelerate

It's now available to treasury management clients in 12 markets in Asia Pacific.

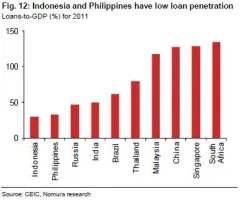

Loan penetration extremely low in ASEAN

Guess which country has the lowest loan penetration at 30% of GDP?

Check out how Citi's new 'smart-banking' machine lets you bank outside of the branch

You can start a transaction on a mobile device and complete it on Citibank Express.

Indonesia has the most profitable banking system in ASEAN: Nomura

Its ROA is forecast to reach 2.7% in 2013F.

OCBC to aggressively boost growth in Indonesia, China

It now has 350 branches in Indonesia.

OCBC Bank suffered from margin pressure

Pressure was evident in Singapore, Indonesia, and China.

2 reasons behind OCBC's weaker underlying banking trends

Margin decline is one culprit.

BNP Paribas aims to grow investment banking revenues in Asia to over 3b euros by 2016

It's a compounded annualised growth rate on the order of 12%.

BPI's profit growth predicted to slow sharply

Blame it on high base from trading gains.

Singapore banks weakest in Asia

Earnings to barely grow 2% YoY.

Here's why large Asian banks have been gaining market share

Current and savings accounts deposits increased 4.9%.

DBS' big boss asserts operating profit growth is realistic this year

But it'll be 'mid-single digit'.

This is how these large Asian banks' deposit market share has increased since 2003

Guess which bank gained the most market share with a 6% growth?

Hong Kong's large banks raked in more deposits than Singapore's

Find out how big the difference is.

Thought Leadership Centre

Most Read

1. Why Thai finance firms push AI as human oversight limits automation 2. Bank of Singapore reshuffles advisory team amidst UHNW focus 3. Banks waste AI spending without workflow redesign as only 10% see gains 4. Why banks must become gatekeepers or accept commodity status 5. DBS Bank taps Ascenda to boost rewards competitionResource Center

Advertise

Advertise

Event News

From insurance to lending, the winners are those doing "less but gaining more" by prioritizing risk-adjusted returns over market share.

Commentary

Perth is emerging as an unlikely testbed for the future of global finance

Buy now, worry later: The hidden cost of BNPL

Why most banks are struggling with AI, and what the smart ones are doing differently