Singapore

Risk management in Islamic banking

Risk management in Islamic banking

Banking in Asia has grown by leaps and bounds in terms of size, profitability, sophistication and maturity in the dozen years so far of the 21st century. One of the standouts in this growth has been Islamic banking. Although Islamic banking has a long and illustrious history dating back to the advent of Islam some 1500 years ago, in its current incarnation it is less than 50 years old. And, as happens in a relatively young industry, there are several debates about its form and substance. One of these relates to risk management in Islamic banking.

Asia hit by shortage of credit and risk professionals

Despite current global economic conditions, demand is still evident across Asia’s banking and finance sector for particular skills. Here Christine Wright, Operations Director for Hays in Asia, discusses trends and current opportunities across the region from the latest Hays Quarterly Report.

Preparing for M&A success in an uncertain environment

With a decline of 16% in deal volumes and 29% in deal values in Q1 2012 over last year, Asia has not been immune to the global reduction in M&A activity over the last few quarters. However, there were still more than 2,700 transactions and $117 billion of total disclosed deal value involving Asian targets or acquirors in Q1 and Asia remains a certain destination for companies looking to gain exposure to fast-growing consumer markets or to assets in strategically important or demographically attractive industries such as energy and healthcare.

Retail banks brace for new wave of technology adoption

Global Banks have a grueling task of repositioning their business portfolio in view of financial upheavals in the wake of European crisis and American journey, to achieve financial freedom. In parallel to this unstable scene, revenue models in retail banking are radically changing, as traditional revenue sources of transaction-driven volumes are drying up and are being replaced with new wave of portfolio-driven revenue propositions, where customers are increasingly expecting banks to guide their financial destiny.

Barclays: Valuation by analysis

We proposed that Barclays should be split into two separate banks - one focused on retail banking and the other on investment banking - in our 5 July Commentary. That presumed, of course, that the investment bank would be viable and able to fund itself on a stand-alone basis in today's challenging markets.

How will Indonesia's new ownership cap rules affect DBS' bid for Bank Danamon?

Analysts believe DBS' acquisition of Bank Danamon is likely to go ahead despite the new regulations - but on what grounds?

Trade finance to be a significant revenue stream in Asia: DBS

Banks may also see opportunities in open account trade or supply chain finance despite economic instability.

ANZ to launch online cash management platform in late 3Q12

ANZ Transactive will allow real-time checking of current balances and approving or rejecting key payments.

DBS' Peter Triggs to focus on private banking for clients in Middle East and Europe

As DBS' new managing director, head of international clients and wealth structuring, Triggs will be recruiting bankers with strong international linkages.

Singapore banks' profit to slump 18% in 2Q12

The large trading gains in 1Q will unlikely be repeated this time around.

Rumours of the death of the bank branch have been greatly exaggerated

The global banking industry is pretty much at an all time low in terms of reputation. Nowhere is this so true as in the UK, where it might have been thought that public opinion of the banks could hardly have sunk any lower in the aftermath of the financial crisis that has enveloped the global economy since 2008. But in the past few weeks a processing malfunction at RBS seriously affected millions of customer accounts, while the Libor rate-fixing scandal that has claimed the jobs of Barclays Chairman, Marcus Agius and Chief Executive, Bob Diamond.

Who's banking Asia's millionaires?

Private banks are in for a competitive market to serve Asia's rich with a whopping wealth of US$10.7 trillion.

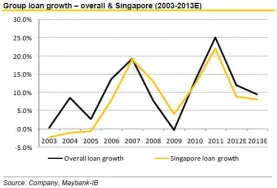

Singapore loan growth to taper off to 8% in 2012

UOB's loan growth is also like to trend towards the lowteens of 10-12%.

How can banks customize their service model to cater to each client's needs?

Bankers say there is no 'one size fits all' solution nowadays.

RBS pulls out of Singapore Libor panel

Royal Bank of Scotland pulled out of a Singapore panel setting interbank lending rates.

Overhauling the weak segments of the Spanish financial sector

Supervision of Spain’s troubled banking system has now passed largely into the hands of inspectors drawn from the European Commission, the IMF, the European Central Bank (ECB) and the European Banking Authority (EBA). This follows agreement by the European authorities to provide Spanish banks directly with up to €100bn of new capital via the EFSF bailout fund.

The difference between a bank's product vs service

Many banks across the Asia Pacific (APAC) geography are implementing Core Banking products. These banks expect that a modern Core Banking product would give them a competitive edge, the ability to launch new products faster, lower operational costs and improve customer service. Unlike Europe or America, which are large with fairly standard banking offerings, the APAC geography is actually characterized by much more variety in its range of offerings.

Thought Leadership Centre

Most Read

1. UOB’s net profit down 16% to $443m in Q3 2. ShaComm Bank, HashKey team up for digital asset push 3. MAS, police tighten coordination for Prince Holding Group probe 4. Hang Seng Bank launches money lock feature 5. ANZ warns H2 profit will be hit with $727.19m charges from significant itemsResource Center

Advertise

Advertise

Events

Event News

Experts explored how hybrid multi-cloud strategies and interconnected data centres are shaping the future of banking in the region.

Commentary

Fighting fraud in the digital banking age

Asian banking’s next frontier: Beyond growth, embracing precision

Rethinking cybersecurity: How APAC banks can safeguard against AI-powered threats

Why Singapore’s fast payments need faster protections