Singapore

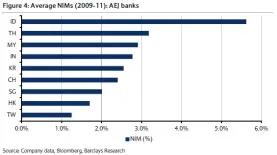

A closer look at AEJ banks' NIMs from 2009-2011

Singapore banks had the biggest margin decline.

Why changing the mindset is as vital for banks as knowing the customer

It’s fair to say that, at the moment, consumer protection high on the agenda of many national regulators and central banks. The global financial crisis has severely dented consumer trust, with the most recent scandal – the LIBOR rate manipulation – dealing a further blow to consumer confidence.

Here's why Asian banks' NIMs will slump

Find out what the two key factors are.

DBS, UOB, OCBC must brace for nastier net interest income pressures

Don't neglect an analyst's warning.

DBS, OCBC, UOB still among the world's strongest banks

The next 12-18 months will be stable.

Visa's Ooi Huey Tyng aggressively eyeing a cashless society

Find out what the new country manager for Singapore and Brunei will do differently in her position.

Fears of profit losses escalate for Singapore banks

Macro headwinds will be the culprits.

Deutsche Bank launches dbIntegrate

It is an outsourced solution providing end-to-end execution, settlement and custody services.

4 signs that Deutsche Bank is strengthening its transaction banking business in Asia Pacific

New initiatives include the Asia Accelerator and FX4Cash.

Banque Internationale à Luxembourg signs MOU with Deutsche Bank

BIL will utilize Deutsche Bank’s Autobahn App Market.

Asian banks urged to build AML compliance programs

Asian banking operations face increasing exposure from regulators around the world to AML regulations – though the pressure locally is diverse in approaches and lacks enforcement. This is particularly challenging because regulators from different Asian countries have different approaches - principle-based versus rules-based - and maturity in their regulatory oversight.

Singapore banks selling non-core investments to prepare for Basel III

OCBC sold F&N and APB while DBS sold its stake in BPI.

OCBC to suffer from rising earnings headwinds

Higher-yielding unsecured personal lending will not be enough to offset higher funding costs.

UOB set to grow in Malaysia, Thailand, Indonesia

But the bank may suffer from currency translation losses.

DBS' acquisition of Bank Danamon bound for integration risks

Find out what other risks loom for DBS.

Singapore banks' deposit market share under threat from foreign banks

They have already increased fixed deposit rates at ~1%.

Thought Leadership Centre

Most Read

1. Why Thai finance firms push AI as human oversight limits automation 2. Bank of Singapore reshuffles advisory team amidst UHNW focus 3. Banks waste AI spending without workflow redesign as only 10% see gains 4. Why banks must become gatekeepers or accept commodity status 5. DBS Bank taps Ascenda to boost rewards competitionResource Center

Advertise

Advertise

Event News

From insurance to lending, the winners are those doing "less but gaining more" by prioritizing risk-adjusted returns over market share.

Commentary

Perth is emerging as an unlikely testbed for the future of global finance

Buy now, worry later: The hidden cost of BNPL

Why most banks are struggling with AI, and what the smart ones are doing differently