The Invoice Data Exchange Accelerates SME Banking Innovation

By Eiichiro YanagawaInnovation opportunities for payment digitalization in Japan.

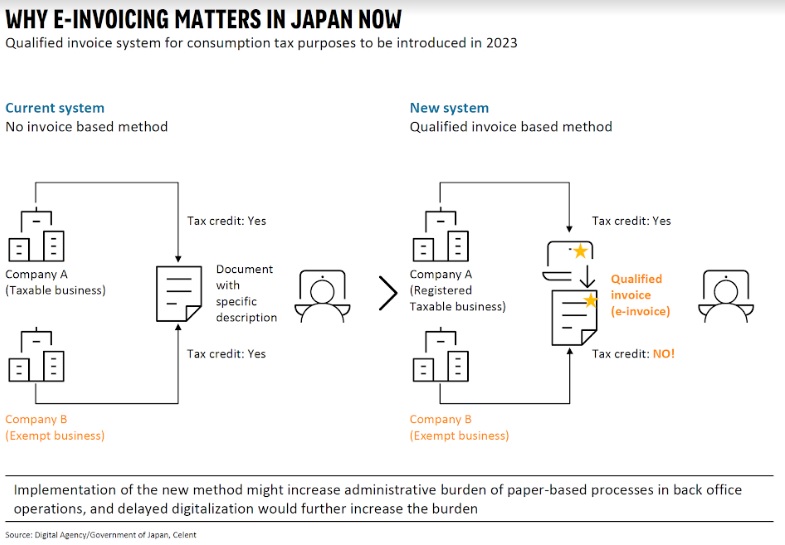

Electronic invoice (e-invoicing) is a system to digitize qualified invoices that are mandatory for the deduction of purchase tax under the qualified invoice system. This invoice system is intended to provide an appropriate consumption tax credit for purchases in response to the multiple tax rates for a consumption tax in 2019 and is scheduled to be introduced in October 2023. When the invoice system starts, only invoices issued by qualified invoicing businesses will be eligible for the purchase tax credit calculation. Invoices issued by others (e.g., tax-exempt businesses) will not be eligible for the purchase tax credit.

The handling of these qualified invoices is expected to create an unprecedented workload for both buyers and sellers, and presents an opportunity for innovation. The government and private sector organizations involved in accounting systems have begun discussions to introduce e-invoicing, or the complete digitization of invoices exchanged between companies, in preparation for the upcoming launch of the qualified invoice system.

Opportunities for innovation

- The Zengin electronic data interchange system (ZEDI) is expected to be a good target use case for e-invoicing. On the other hand, the use of ZEDI alone cannot fulfill the preservation requirements of the Act on Special Measures for Preservation of National Tax-Related Books and Documents Prepared Using Computers, “The Act on Electronic Preservation Books/Documents.”

- Therefore, to utilize ZEDI for electronic invoicing, it is essential for a company's accounting/ERP system to be ZEDI-compliant. The issues are retention period, readability, and retrievability, all of which provide opportunities for innovation. ZEDI is a system for receiving and sending message telegrams, and the EDI data storage, readability (ZEDI is encrypted data), and searchability are not sufficient to support electronic invoicing operations.

Targets of innovation

- Japanese policymakers and market participants should refer to precedents in European markets. In 2010, the European Union issued a directive requiring that electronic invoices have the same legal status as paper invoices, and that the authenticity and integrity of electronic invoices be supported by electronic signatures as well as technologies such as electronic data interchange (EDI).

- The EU then issued an additional directive in 2014 requiring member states to receive and process electronic invoices for public contracts between companies and governments (B2G), along with common European standards. Due to fragmentation by countries and providers, PEPPOL (Pan-European Public Procurement Online) was established in 2011.

- PEPPOL is not an eProcurement platform, but rather a set of technical specifications that can be implemented in existing eProcurement solutions and business exchange services to enable interoperability between heterogeneous systems. PEPPOL is based on three main pillars: the network (Peppol eDelivery Network), the document specifications (Peppol Business Interoperability Specifications - BIS), and a legal framework defining network governance (Peppol Transport Infrastructure Agreements - TIA).

- Three keys to success around e-invoicing, based on European precedents:

- There are many B2B / supply chain networks around the world. Many network providers offer certified PEPPOL access points, which are communication nodes on the network, and interoperability is key.

- Onboarding of suppliers to the buyer's chosen B2B network is critical, i.e., having suppliers register with the network and upload their invoices to a common portal. Large buyers want to ensure integration with downstream ERP and procurement systems. For technology vendors, consider becoming a certified PEPPOL provider or partnering with an established global player that supports cross-border invoicing.

- Most firms deal directly with electronic invoicing vendors. This is because banks do not play a significant role in the areas of order-to-cash (O2C: accounts payable processing) and procure-to-pay (P2P: accounts receivable processing). In other words, it is an "untapped service area" for banks, and obtaining the "platform position" is expected to be the main battleground for fintech alliances in the future.

Innovation in action

- Among Japanese companies, 99.7% are small and medium-sized enterprises (SMEs).

- Increasing sales is the top priority for any business, but at the same time, SME owners face various financial and non-financial concerns. According to Celent's "SME Market Survey," the challenges faced by SMEs currently diverge from those experienced by financial institutions. In addition to improving sales in existing channels, there is a strong interest in digital platforms to improve overall commercial activities.

- For SME banking, offering financial services that can be seamlessly integrated with online accounting solutions is a top priority. The key is to negotiate the desired scope of data access with accounting service providers and present SMEs with compelling reasons and benefits to agree to share their accounting data with banks.

- To re-enter the new SME banking space, bankers need to re-evaluate their existing strategies and accelerate their use of technology. On the other hand, the new business model creates new opportunities for all players, including attacker banks and fintechs, to challenge traditional corporate banks or collaborate with disruptive challengers.

The winners in SME financial services will look different from today's banks.

- They will take a customer-centric approach and offer simpler accounting workflows, smarter financial data analysis, and actionable financial and non-financial advice, rather than the banking products themselves, and thus embed banking products and services within a broader SME offering.

- To be a pacesetter in a tough competitive environment, banks need to go beyond incremental change. To achieve step-change and execute a game-changing move, they need to offer "embedded financial services" instead of selling stand-alone "banking services."

- This means integrating their financial product services into the workflow of SMEs and enhancing their data analytics offerings using third party data, and their embedded product services span the service areas of payments and credit for SMEs.

Advertise

Advertise