Greater Bay Area loan access index sinks to 48.7 as recovery reverses

Quarterly business confidence data shows lending conditions falling back into contractionary territory.

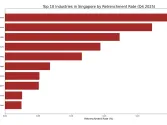

Credit and liquidity conditions tightened further in the fourth quarter of 2025, according to a survey of companies in the Greater Bay Area.

The “Standard Chartered GBA Business Confidence Index”, jointly presented by Standard Chartered and Hong Kong Trade Development Council, revealed that the current performance index for credit slipped to 48.7, reversing the modest improvement seen in the third quarter.

Respondents said access to bank lending became more difficult compared to the previous quarter.

The sub-index tracking banks’ attitude towards lending fell by 2.7 points to 46.9, making it one of the main factors pulling down the overall credit index.

Bank financing costs continued to rise, though at a slower pace than in the third quarter, with the relevant sub-index increasing by 2.2 points to 49.6.

By contrast, funding costs from non-bank financial institutions eased further, with the sub-index edging above the 50 mark, indicating expansion.

Liquidity conditions also weakened in the fourth quarter, as both surplus cash and receivables turnover moved deeper into contractionary territory.

Enhanced transaction banking efficiency could free up liquidity by reducing funds in transit and capital tied up in for pre-funding of payments,according to a July 2025 report by ISDA and Ant International under Project Guardian on Foreign Exchange (FX).

“However, it is imperative to address the potential fragmentation of the liquidity pool and fungibility of liquidity pools arising from programmability of tokenised bank liabilities,” the report stated, which focused on the use of tokenised bank liabilities and shared ledger in cross-border payments.

Tokenised bank assets can also streamline cross-border payments and FX settlements, which in turn could minimise counterparty and settlement risk.

Looking ahead, surveyed companies expect credit and liquidity conditions to tighten further in the first quarter of 2026.

The sub-indices for banks’ attitude towards lending, surplus cash and receivables turnover are all expected to remain in contraction.

At the same time, respondents anticipate financing costs from non-bank financial institutions to fall further from fourth-quarter levels.

Advertise

Advertise