Corporate acupuncture: How precision M&A is reshaping Asia’s competitive edge

By Nicole ZhouMomentum is coming from targeted, capability-led acquisitions.

Whilst billion-dollar blockbusters dominate headlines, a growing number of Asian companies have quietly mastered something different: strategic, programmatic acquisitions that deliver superior returns by prioritising speed, capability integration, and precision over pure scale.

Corporate M&A has long been synonymous with size. Bigger is better. But look closely at what’s happening across Asia-Pacific, and you'll see a fundamentally different playbook – one that is delivering measurably superior outcomes by avoiding the complexities often associated with megadeals.

Call it “corporate acupuncture”: Asia’s most strategic acquirers are using programmatic M&A – multiple smaller, more targeted acquisitions – to build cross-sector capabilities, integrate specialised technologies, and capture value faster. These aren’t tiny needle pricks; they’re strategically placed investments hitting exactly the right pressure points to unlock disproportionate advantage.

And the data proves it works.

The numbers tell the real story

Companies following a programmatic approach – pursuing more than three small or midsize deals per year – are delivering total shareholder returns 3.5% above industry benchmarks. That’s the sustained competitive advantage built through disciplined, repeated execution.

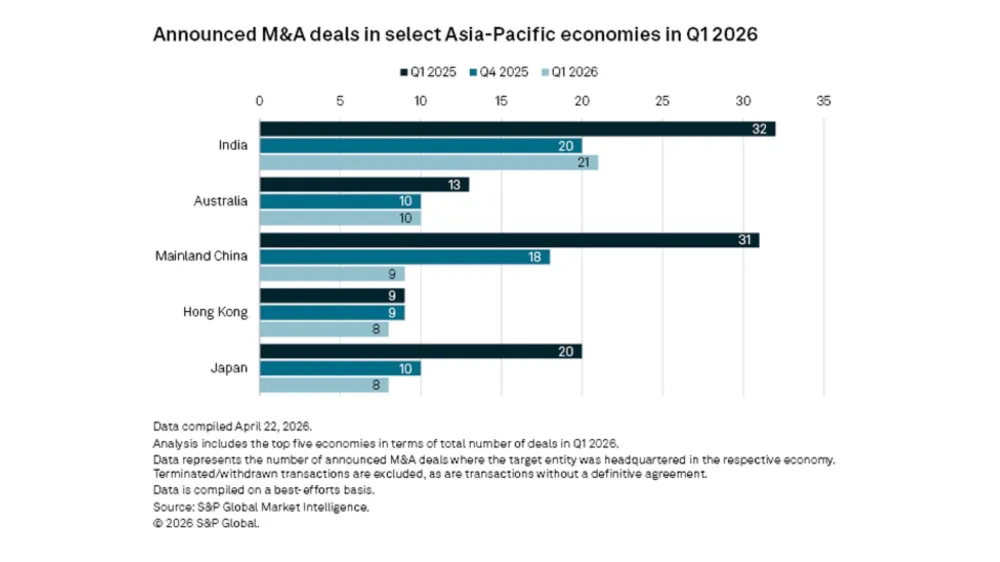

In Asia-Pacific, a continued focus on midmarket deals means transactions are smaller, but integrations are simpler, and return on equity can be larger. India saw deal value rise 16% in 2025 to $162b (US$99b), driven by targeted capability acquisition across sectors. The global secondaries market surpassed $207b (US$162b) by the third quarter (Q3) of 2025 – clear evidence investors prefer liquidity and speed over blockbuster bets.

Even in defense and aerospace, more than 80% of corporate deals in 2025 were under $1.281b (US$1b). Corporations will continue pursuing small to midsize deals as larger consolidation opportunities remain limited.

Why strategic precision beats pure scale

Momentum is coming from targeted, capability-led acquisitions – particularly in technology and artificial intelligence (AI), where success relies on integrating capabilities and reshaping workflows. This isn’t about buying market share; it’s about acquiring precise technical talent, intellectual property, or platform capabilities that solve immediate problems whilst building long-term advantage.

The watchwords for 2026 are “smaller” and “more strategic” – dealmakers prioritise targets offering thematic fit, technology alignment, and quickly captured value. Success requires rapid technology integration and capability building – exactly where programmatic acquirers excel.

Companies are investing across semiconductors, AI infrastructure, electric vehicles, battery manufacturing, renewable energy, and critical minerals. These aren’t vertical consolidations – they’re horizontal capability plays creating ecosystems rather than monoliths.

The programmatic advantage: speed, discipline, repetition

Programmatic acquirers achieve higher total shareholder returns alongside lower long-term risk. Their approach – more than two deals per year with meaningful market capitalisation – allows them to continually refine M&A playbooks and synergy blueprints.

By late 2025, sponsors demonstrated greater discipline, adapting to a financing market supportive of smaller deals. Private equity now accounts for one-third of tech sector deal value, favoring bolt-on acquisitions that provide recurring revenue and bolster intellectual property.

Consider the strategic positioning: Tata Motors’ $14.09 (US$11b) acquisition of Iveco adds European manufacturing expertise. SoftBank’s $8.3b (US$6.5b) investment in Ampere Computing positions Japanese capital behind semiconductor innovation critical to AI infrastructure. These are capability-focused moves, not consolidation plays.

IT firms are acquiring specialised AI startups – transactions that tend to be smaller but remain strategically critical. Investors increasingly target cold-chain, healthcare, electric-vehicle battery, semiconductor, and aerospace logistics providers.

The integration advantage some are missing

Strategic, programmatic deals integrate faster, capture value sooner, and reduce execution risk through repeatable processes.

Companies using AI in M&A activities report 20% cost reductions and 30 to 50% faster deal cycles. One corporate development team identified and scored over 500 potential targets in under a day, prioritising 15 deal leads that culminated in three completed acquisitions within months.

That’s the programmatic advantage: develop sharp, repeatable processes; move quickly; integrate efficiently; do it again. Organisations building end-to-end M&A capabilities – with dedicated teams, repeatable playbooks, and governance supporting rapid decision-making – are best positioned to convert strategic intents into sustained performance.

When geopolitical shifts occur, acquirers with detailed M&A blueprints can change course efficiently. Leading Asia-Pacific companies have reimagined strategies to find growth, gain capabilities, build resilience, and mitigate risk in a complex world.

What Fortune 500 companies stand to lose

Whilst some enterprises spend years negotiating and integrating, Asian competitors execute programmatic strategies – making multiple strategic acquisitions that solve specific problems and open new markets.

Asian investors have increased outbound activity in Australia and North America, bringing programmatic discipline to global markets. The gap widens as Asia-Pacific companies make strategic bets on technologies and capabilities defining the next decade, whilst some firms pursuing megadeal strategies find themselves outpaced by rivals with more specialised, integrated, and adaptable ecosystems.

Private equity sponsors are following suit, leaning into synergy-driven plays including rollups and “string of pearls” strategies. The emphasis is on targeted add-ons, operating leverage, and adjacencies.

This isn’t about geography – it’s about methodology. The shift toward smaller, strategic, capability-led acquisitions with programmatic discipline represents a fundamental evolution. Those who adapt will thrive. Those who wait for the “right megadeal” will find themselves disrupted by competitors who moved faster, integrated smarter, and built stronger capabilities through dozens of strategic acquisitions.

The Fortune 500 has a choice: adopt programmatic M&A strategies prioritising speed, capability integration, and repeatable excellence – or keep watching companies that have already moved on to their next three acquisitions whilst you’re still integrating your last megadeal.

Strategic precision beats brute force consolidation. The data proves it. The question is whether organisations will adapt before it’s too late.

Advertise

Advertise