Economic crises can be avoided by using the Islamic financing paradigm

By Md. Touhidul Alam KhanFinancial system based on shariah, or Islamic law, is a better strategy than traditional finance in light of the recent difficulties in the global economy. The area of the global financial system with the quickest growth has been Islamic finance. Because of the high level of innovation that has kept up with the changing demands for financial products and services as economics continues to change and expand, this growth has also been in quality and depth. The increased availability of profit-loss sharing savings, investing, and other structured finance-based instruments is significant.

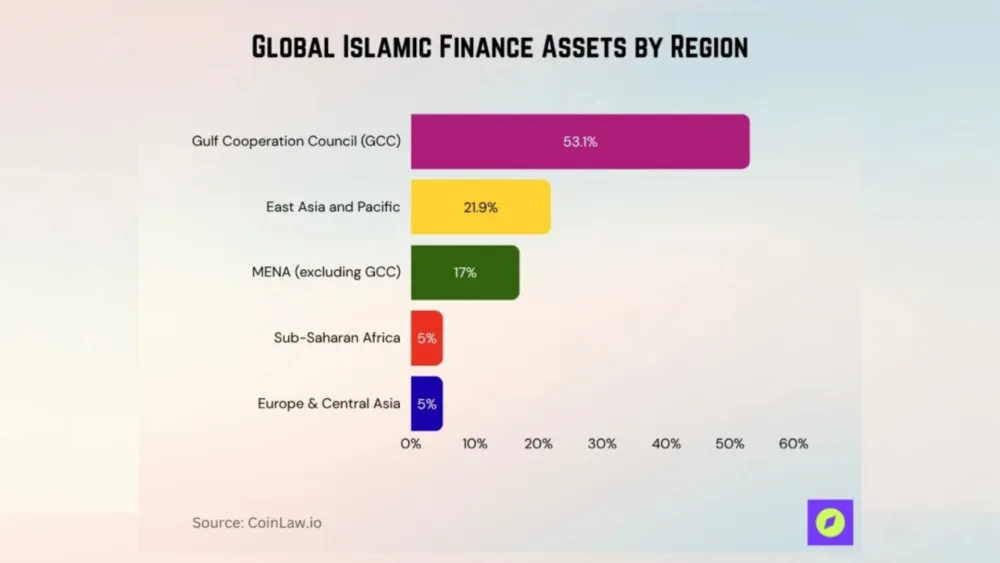

The global assets for the Islamic industry grew to $3.374 trillion in 2020 and it is anticipated to an 8% average yearly growth until 2025 which will reach to $4.95 trillion. These amazing advancements have shown that Islamic finance has the ability to effectively supply financial intermediation to fulfill the demands of a contemporary, globally integrated financial system and economy. The significant and quick development of Islamic finance highlights the need for greater focus and attention on issues of prudential regulation, risk management, and overall financial stability in order to prevent any future economic crisis, even though Islamic finance has repeatedly demonstrated its resilience and sustainability during the global fiscal crisis. Issues regarding the supervision and regulation of banks and financial institutions, including Islamic Financial Institutions, have become more clear and understandable things to the evolving compendium of standards, codes, and principles from the Basel Committee on Banking Supervision, the Financial Stability Board, and other international standard-setting bodies.

“O you who have believed, do not consume one another’s wealth unjustly but only [in lawful] business by mutual consent. And do not kill yourselves [or one another]. Indeed, Allah is to you ever Merciful”. [Surah An-Nisa; Ayat 29 (4:29 Al-QURAN)]. That means it is a clear declaration that Islam authorizes only for lawful business. It indicates that Islam is more than a “religion” in the common restricted sense and it is more of an all-encompassing manner of life.

There are approximately 1.9 billion Muslims globally and Islam has given us a proper mechanism and guidelines for living and doing fair business. We must have strong belief and faith that every guidance has underlying moral values and benefits for us. The Shariah framework to conduct business encourages us to comply with fair and ethical practices. These Islamic teachings are not just for Muslims; they are equally significant and helpful for anybody who wants to engage in moral behavior, fair trade, and values promotion.

A business should trade only that which is lawful. Items such as alcohol, tobacco, pork, pornographic material, and services, and interest-based (‘Riba’) debts should not be traded. The unlawful items in Islam are known to cause damage to individuals and society physiologically, economically, morally, and spiritually.

Islam provides clear instructions on maintaining integrity and being truthful in all spheres of life. However, since the risks are greater, there is a greater emphasis on maintaining honesty and integrity in business. However, trust plays a significant role because there is an informational imbalance between the vendor and the buyer. As per hadith (Sunan al-Tirmidhi), "The honest and trustworthy merchant will be with the prophets, the truthful, and the martyrs."

A fundamental rule of Islamic business is the effective treatment and timely payments to employees. The Prophet (peace be upon him said) said: "Give the worker his wage before his sweat dries." [Ibn Majah]. Allah says, "O you who have believed, fulfil your contractual obligations." [Quran 5:1]. This verse highlights the importance of both parties abiding by their side of the bargain. On one occasion, the Prophet reports that Allah said: "I will be the opponent to three types of people on the Day of Judgment: and one who hires staff, takes full work from them and does not pay them their wages." [Sahih al-Bukhari]. Staff should be well-served in addition to receiving payments on schedule. According to studies, when employees are treated well, they are more productive and loyal, which increases an organization's output, growth, and profitability while also increasing staff retention and lowering staff turnover rates. Additionally, it helps to foster deeper customer interactions and supports a larger talent pool of employees at all levels of the workforce.

One of the fundamental tenets of Islamic commerce is to value the counterparty and protect their integrity. Islam forbids lying and cheating when conducting business. This concept guarantees that we value and respect the people we trade with, in addition to being honorable in our dealings. The Prophetic narration states: "Whoever cheats us, is not one of us." [Sahih Muslim]

The Prophet advised traders and businesses to give charity. He said: "O Businessmen, transactions carry lies and false oaths, so add charitable giving to your businesses [to mitigate wrongdoing]." [al-Nasa'i]. The charity has not yet included the financial side, but it is also committed to addressing climate change, trying to reduce waste, and implementing a zero-waste economic model. The charity also includes looking out for the environment, supporting the blue and green economies, and using a business strategy that advances the Sustainable Development Goals (SDGs).

Islamic financial institutions ought to support and carry out legal trade and asset-based investment. Policymakers should encourage charity-based funding, charity models, use of block chain in charity, etc., and provide guidelines on its operational process and mechanism. Islamic doctrine focuses on wealth distribution (Zakah, etc.), increasing aggregate demand, and encouraging participation in business activities through saving and investment. Muslim economies should work together to support one another and create a different economic system from the established one.

As per Islamic finance model, production is restricted by some conditions: (i) The product or service must be lawful, (ii) The method of production should not cause an undue and excessive harm to Allah-given resources and bounties for the benefit of all mankind. (iii) Productive resources are not to be left idle in the name of private ownership, especially resources that are crucial to the lives of people, (iv) The production process should not cause harm to others and also allowing the maximum possible “information” about the going prices of goods to be disseminated so as to allow the seller to get the best and fairest price for his products. At the time of the Prophet, some middlemen used to go to the outskirts of the town [where there is a frequented market] where they intercept out-of-town merchants or farmers who are bringing their products to sell in the market. These middlemen would then offer to buy such products at a given price which was commonly less than the going market price. The Prophet forbade that practice and instructed that the sellers should be allowed to get to the market first [i.e., to find out the going or offered price for their products] before an offer is made to them. From an economist’s perspective, it is a case of enhancing information among the buyers and sellers. This improves the competitive nature of the market and thus help determine the “equilibrium” fair price.

Although there is a strong connection between Islamic financial institutions around the world, the integration of global institutions will provide Islamic financial institutions a new role that will enable them to support one another in financial inclusion. International organizations will then be able to comprehend the problems and difficulties faced by a nation's Islamic financial institutions, which will help another nation learn how to deal with similar difficulties.

Today's buzzword for the world's economies is fintech. Global economies are finding new avenues for creative financial solutions thanks to the acceptance of fintech and its ramifications. Fintech also has advantages for Islamic banking, although its full social impact has not yet been realized. Thus, Islamic financial institutions should focus on promoting Islamic fintech adoption through aggressive strategies and the most straightforward methods for fintech users.

Academics, researchers, decision-makers, and scholars of Shariah have the authority to recognize the issues and difficulties that are unique to a given nation or geographic area with regard to the Islamic financial system. This action will help resolve concerns with Islamic money on a worldwide scale. It has been contended that the subprime loan crisis and the failure of some of the greatest banks in the world may have been prevented if the globe had adhered to the real principles of Islamic finance. Under Islamic finance model to sustain long-term growth, Muslim countries must liberalize their economies, embrace efficient institutions, and adopt consistent macroeconomic policies. They need to grow on a sustained, more rapid basis, and address all prominent issues of social and economic justice under Shariah. The most significant driver of a prosperous Islamic finance sector and equity-based assets more broadly would be their consistent economic growth. We think that the Shariah-based Islamic business model, which is moving more and more in the direction of faster economic growth and the expansion of the financial market, is beginning to show signals that Islamic countries are ahead of other non-Muslim countries. Thus, it is simple to state, by utilizing the Islamic financing paradigm, economic catastrophes can be averted.

*****

Md. Touhidul Alam Khan is the Additional Managing Director; Chief Risk Officer and Chief Anti Money Laundering Compliance Officer of Standard Bank Limited, Bangladesh. He is Fellow Member of Institute of Cost & Management Accountants of Bangladesh (ICMAB) and first Certified Sustainability Reporting Assurer (CSRA) in Bangladesh.

Advertise

Advertise